… and what it will mean for Sole Traders and Landlords

The government’s ongoing programme to make the tax system fully digital has been delayed for 12 months. HMRC announced the delay in October in recognition of the impact that the pandemic has had on British businesses.

Making self assessment digital will predominantly affect people who are Sole Traders and Landlords.

What will sole traders and landlords have to do?

From April 2024, individuals currently using self assessment for their income tax will need to use digital methods for their income tax accounting and reporting. This involves:

Registering for Making Tax Digital for Income Tax by 6 April 2024

Adopting an accounting software system that is compatible with Marking Tax Digital for Income Tax.

Providing HMRC with quarterly updates using your software.

Submitting an End of Period Statement by the end of January and a final declaration of all your income.

Paying the balance of any tax and National Insurance contributions due.

Does this affect all landlords and sole traders?

Landlords only need to follow the Making Tax Digital rules if the rent they receive is more than £10,000 per year..

It will not affect landlords who set up a limited company for their property business, as these will pay corporation tax. Making Tax Digital for corporation tax will not arrive until at least 2026.

On a similar note, Making Tax Digital will apply to any sole traders whose income is more than £10,000 per year. If you are under the £10,000 threshold you will be able to continue to file your tax return in the normal way.

Are there any exceptions?

There is an option to apply to be ‘digitally excluded’ if it is not practical or possible for you to use a compliant software system. This might be due to disability or a lack of cloud connectivity where your business is based. You will need to evidence your reasons to HMRC.

Is there a way to make this simpler?

If you don’t already have an accountant, now may be a good time to appoint one. We will recommend a suitable accounting system that is compatible with Making Tax Digital.

While you will need to input your income and expenses into the system, your accountant can work out your quarterly updates, End of Period Statement and final declaration. We will also make sure you keep to all the deadlines.

Although there is no rush to move to a cloud based system just yet, the sooner you get used to a new accounting system, the more confident you will feel by the time the new requirements become law.

We’re happy to talk you through Making Tax Digital and what’s involved. We’re accountants for Sole Traders and landlords across the Lune Valley area. We also manage payroll services and corporate accounts. Just get in touch!

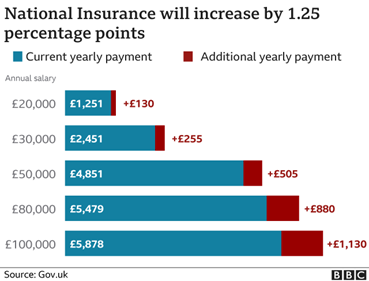

Earlier this month, Boris Johnson announced a new health and social care tax to fund reforms to the care sector and NHS funding. It is set to raise £36bn for front line services over the next three years.

The tax will begin as a 1.25% rise in National Insurance from April 2022. It will be paid by both employers and employees. From 2023 it will become a separate tax on earned income, calculated in the same way as National Insurance and appearing on an employee’s payslip.

The Prime Minister also announced an equivalent increase to dividend tax to help cover social care costs.

What’s the purpose of the new tax?

The Prime Minister says that part of the £12bn a year will support the NHS to catch up on the backlog created by COVID-19, increasing hospital capacity for appointments, scans, and operations. The money will also go towards changes to the social care system. A new cap to care costs is to be introduced from October 2023. The maximum any individual will pay in care costs will be £86,000 over their lifetime.

Everyone with assets worth less than £20,000 will then have their care fully covered by the state. People with between £20,000 and £100,000 in assets will see their care costs subsidised.

What does the increase mean to working individuals?

As shown in the diagram below, taken from the BBC website, an individual earning £20,000 will now pay an additional £130 per year in National Insurance. Someone on a £50,000 salary will pay a further £505 per year.

What does it mean to employers?

Employers will need to re-budget to allow for these additional employer’s National Insurance costs. Note that existing reliefs on NICs, including the employment allowance, will also apply to the levy.

Some options to consider include:

Exploring share option schemes rather than bonuses for higher earning employees.

Salary sacrifice as an even more efficient way of making pension contributions – this reduces the salary on which employer and employee NICs are paid.

What does it mean to shareholders?

The equivalent increase to Dividend Tax will mean a similar impact to limited company owners and savers.

To mitigate this increase, small business owners could declare increased Dividends before April 2022.

The switch to electric vehicles is well underway, which spells good news for CO2 reduction and pollution in the UK. There are now more than 260,000 electric cars and 535,000 hybrid models on our roads.

The UK government is actively promoting the purchase of electric vehicles as part of its commitment to reach Net Zero by 2050. It has already announced that new petrol and diesel cars will no longer be sold in the UK by 2030.

In addition, the government has introduced incentives for both businesses and individuals to adopt electric cars and commercial vehicles.

Plug In Grants

A government scheme allows individuals to buy low-emission vehicles with a plug-in grant. The grant covers up to 35% of the purchase price for various vehicles, up to a maximum of £2,500. A list of the vehicles involved is available on this page. The grant is automatically applied to the purchase price when you visit a car dealer.

Vehicle tax breaks

Vehicle Excise Duty is calculated based on CO2 emissions, which makes electric vehicles exempt as they produce zero CO2.

For plug-in hybrid vehicles, owners pay tax in line with the level of CO2 produced – all the details are listed on the government website.

Electric vehicles are currently exempt from the additional £335 in vehicle tax for cars with a list price exceeding £40,000.

Company car tax breaks

A well-known drawback to company cars is that they often create more personal tax liability than they save in corporation tax. Employees who have company cars pay tax on company benefits (Benefit in Kind) of up to 37%.

But if the employee uses a purely electric company car, the Benefit in Kind rate is set at 1% in 2021/22, rising to 2% in 2022/23. This tax rate offers major savings compared with standard vehicles. To calculate your company car/fuel benefit, visit the HMRC website.

Electric Vans

There is also a 1% Benefit in Kind charge for employees who drive fully electric vans and use them privately. The road tax on electric vans is zero.

If you’re looking into electric vans, tread carefully, as not all ‘vans’ qualify as such. Make sure that the vehicle you choose is eligible for tax breaks.

Benefits when driving in Central London

Electric vehicles are an attractive option for those who regularly drive in London, as zero-emission vehicles that meet specific criteria gain a 100% discount on the Congestion Charge. Clean Air zones are also in place in Bath, Birmingham and, from late 2021, Portsmouth. Some London boroughs free parking or discounted parking for electric vehicles.

To discuss ways you can benefit from tax cuts on electric vehicles, get in touch. Our accountancy services in the Lune Valley include personal and business tax planning. We’re trusted accountants for small businesses and individuals, and will be pleased to advise you.

All limited companies pay Corporation Tax on an annual basis. How does it work, and how will the new Super Deduction offer benefits for UK businesses?

What is Corporation Tax?

Corporation tax is paid by UK limited companies and is based on annual profits. Certain expenses can be deducted, and various allowances can help reduce your tax liability.

Corporation tax applies to:

Trading profits – the earnings from doing business

Investments

Selling assets such as land, property, shares, and machinery

Who pays corporation tax?

Corporation tax is paid by all UK limited companies, but not Sole Traders and partnerships. These fill out a tax return and apply income tax to their earnings. Some non-limited organisations do pay Corporation Tax, such as charities and associations.

How much is corporation tax in the UK?

The main rate is set at 19% for all business profits and will remain at this level until 2023.

From April 2023, if your taxable profits are above £250,000 then corporation tax will be payable at 25%. If your profits are £50,000 or less, they will remain at 19%. For profits between these limits, you’ll pay a marginal rate of effectively 26.5% – but with the benefit of marginal relief.

When does corporation tax have to be paid?

Your corporation tax is paid annually, before you file your company tax return. The date it is due therefore depends on your corporation tax accounting period.

You must settle your corporation tax bill nine months and one day after the end of your accounting period from the previous financial year.

Corporation Tax Relief – Expenses

There are various business expenses that you can deduct from your company’s income before calculating the annual profit on which you will be taxed.

These include things like marketing costs, insurance, equipment, training, travel and pensions.

Corporation Tax Relief – The Super Deduction

In the Budget 2021, the Chancellor announced the Super Deduction, a new tax allowance to support business investment.

It was announced as ‘the biggest business tax cut in modern British history’. It is certainly a generous allowance, where a company can claim back 25p for every £1 invested in qualifying machinery and equipment.

It’s only a temporary measure, though, available from 1st April 2021 until 31 March 2023. If you are planning to invest in your business, it is worth prioritising these investments to take advantage of this new allowance.

How do I work out the Super Deduction?

Companies generally claim for assets at 100% of their value to get tax relief. So, with Corporation Tax at 19%, the tax relief on an asset worth £10,000 is 19% of its full value – or £1,900.

But the super deduction allows you to claim relief on 130% of the asset’s value. So, the tax relief of an asset worth £10,000 would be calculated on 130% of its value. From a tax perspective your asset is now worth £13,000, and you get tax relief of £2,470 (19% of £13,000 is £2,470).

The headline figure of 25p per £1 comes from the fact that 19% of 130% of an asset’s value is roughly the same as 25% of 100% of its value.

Who is eligible for the super-deduction?

Any business that pays Corporation Tax is eligible for the super-deduction. It’s seen as particularly appealing to companies in the manufacturing, farming and construction industries.

What qualifies as plant and machinery?

HMRC haven’t released a formal definition of the assets covered by the Super Deduction. But as most tangible assets for a business are considered ‘plant and machinery’ from a tax point of view, qualifying assets generally include:

IT equipment and servers

Office chairs and desks

Tractors, lorries, vans

Ladders, tools

Electric vehicle charge points

Cranes

Refrigeration units

Compressors

What assets don’t qualify?

You can’t claim for cars, shares, or residential property. You can only claim on assets purchased as part of a property if you buy the property brand new, direct from the developer.

You must not have entered the contract to purchase any asset before 31 March 2021.

Are second-hand or buy-to-rent assets included?

No – the Super Deduction only applies to new plant and machinery, and you cannot use it for equipment you’re planning to rent out.

HMRC has confirmed that the Super-Deduction can be used on equipment purchased via hire purchase finance, as long as you are given ownership of the assets under the agreement.

Does the Super Deduction help address the planned Corporation Tax rise?

The Super Deduction is essentially an incentive for businesses to invest in equipment, which in turn will help boost the economy.

Businesses that take advantage of the super deduction will essentially be able to get tax relief at the future 25% rate early, as shown in the table below.

With the super-deduction, before Corporation Tax increases

Without the super-deduction, after Corporation Tax increases

Asset value

£10,000

£10,000

Claiming tax relief on

130% of the assets value = £13,000

100% of the assets value = £10,000

Corporation Tax

19%

25%

Corporation Tax relief

19% of £13,000 = £2,470

25% of £10,000 = £2,500

How to get corporate tax advice

Corporate tax planning can be complex, especially if you’re a small business owner without an extensive finance team. Here at Wootton Co in the Lune Valley, we’re highly experienced in providing corporation tax services as business accountants. Let us help you explore how you can plan business investments to take full advantage of the Super Deduction and other tax allowances. Contact us.

Once you’ve submitted your tax return you’ll know how much you owe HMRC. But how and when do you need to pay? We’ll talk you through Payment on Account and the deadlines.

When to pay your Self-Assessment Tax

Self-assessment Payment on Account applies to UK taxpayers where less than 80% of your income has tax deducted ‘at source’. That means your tax is paid before you receive the money, such when an employer pays an employee under the Pay As You Earn (PAYE) system.

What is Payment on Account?

Payment on Account is the UK system for settling tax the tax owed. The payment is spread over two instalments during the year, based on the previous year’s tax bill.

Essentially, you make an advance tax payment to make sure you never fall behind and end up in debt to HMRC. If your tax liability ends up being higher than the previous year, you may need to make a further payment to keep your tax in balance.

When do I have to pay my tax bill?

If you use Payment on Account, the first payment date is midnight on 31 January. Because this is prior to the end of the tax year, it’s calculated by looking at your previous year’s tax bill.

The deadline for the second instalment is midnight on 31 July, after the end of the tax year in question.

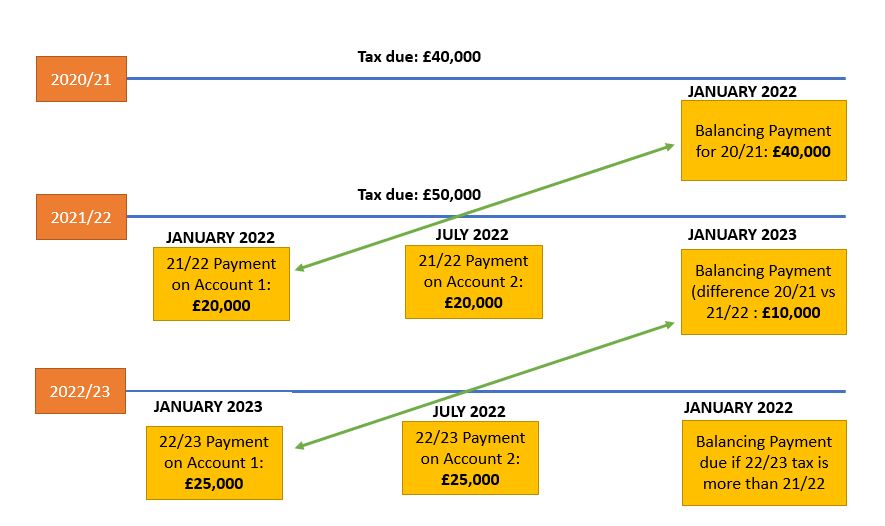

Each instalment is usually 50% of your previous tax bill. Here’s an example:

Tax Bill for year ending April 2021

£40,000

Payment due on 31 Jan 2022

£20,000

Payment due 31 Jul 2022

£20,000

But what happens if you need to make a balancing payment?

Using the example above, let’s say your total tax owed for the 2021/22 tax year comes in at £50,000. That means you have an outstanding balance of £10,000 (£50,000 owed minus the £40,000 paid by 31 July). This is called the balancing payment. It has to be settled by 31 January 2023.

So your 2022/23 payment plan would work as follows.

The main thing to note here is that each January you need to schedule in two fairly large tax payments – the balancing payment from the previous tax year AND the first Payment on Account for the current tax year.

Exceptions to the rule

There are some situations where you won’t have to make two Payments on Account in a tax year. These include:

Where you’ve already paid 80% or more of the total amount of tax you owe

Your self-assessment tax bill is £1,000 or less

What happens if your tax bill decreases year on year?

If you earn a lot of income one year and it drops considerably the next year, it can rightly cause you some concern – because you will potentially have to make a large payment in a year where your income has fallen. So, if you recognise that your next tax bill will be lower than the previous year, it can help to ask HMRC to reduce Payments on Account.

This needs careful consideration, though, because if you end up underpaying, HMRC will charge you interest and could apply penalties. On the other hand, HMRC will refund any overpayments.

How to pay

You can make your tax payments via:

Online banking

Telephone banking

CHAPS or BACS

Direct debit card online

At your bank or building society

At the post office

It can take 3 working days to process a payment via BACS, direct debit and cheque (upon receipt). If you haven’t set up a direct debit arrangement, the first payment will take 5 working days.

You can access what you owe HMRC through its online services. The portal provides you with the payments you need to make in January and July. It also gives you access to historical payments on account.

Top tax tips

Tax can be complicated, but here are some golden rules to help you avoid any issues:

1. Put money aside regularly or find an advisor to help you create a tax payment plan.

2. Get your tax return in early – near the deadline there is more pressure on HMRC’s helpline and support.

3. Check the details carefully for errors.

4. Appoint an accountant to do the hard work for you!

For any concerns or support about hour self-assessment tax returns, get in touch. We provide a full range of accountancy services in The Lune Valley including personal tax planning. We’re trusted accountants for sole traders and small businesses of all kinds. Give us a call and we’ll explain how we can help.

A healthy cashflow is crucial for small companies to navigate the ups and downs of business. Improve cashflow to help you plan ahead, budget for future spending and handle the unexpected.

If you want to get your business to a better cashflow position, here are seven steps to success.

1. Start forecasting

Take time to look ahead, and you will better understand the cycles and trends within your business. It’s good to take a year-long view, so plan out the costs that your business will need to cover: salaries, stock, equipment, rent, tax etc. over the next 12 months. Then estimate your monthly income for the year.

Work out the difference between the two, and you’ll see how your profits look month by month. This information will help you plan in other spending when your business is in the strongest cash position.

2. Credit control

Keep on top of your invoicing, make sure each bill states your payment terms and follow up any late payments promptly. The best way to get a customer to pay up is to become a nuisance! Don’t be afraid to call and email to chase up a late payer – this is your money and should be sitting in your company account, not theirs.

3. Increase supplier payment terms

A great way to improve your cashflow is to negotiate longer payment terms with your suppliers. Not everyone will agree to this, but if you can extend a term from 30 to 45 or even 60 days, you will have more flexibility with your bills. That way you can pay once income has arrived from your customers.

4. Automate your systems

The power of accounting software can’t be understated. If you aren’t already using online tools to manage your invoicing, tax and banking, take a look. These systems are easy to use, highly efficient and will save you time and money.

5. Stock management

Having too much stock can mean pressure on storage and a cashflow deficit – but not enough stock can affect your supply chain and customer relationships. Taking charge of your inventory is an important step in cashflow management.

6. Reduce your costs

It’s important to take a regular look at where your money is going and whether there are savings to be made. Often fixed assets and monthly subscriptions can add up.

Checking whether you can get a better deal on telephone systems, IT and insurance can often save considerable amounts. Look too at company vehicles and other assets – are their options to lease them rather than own outright?

7. Prepare for the worst

… and hope for the best. It’s always worth having a backup plan in case things go wrong or something unexpected happens. Do you have a credit facility with your bank? How would you manage if you suddenly needed to outlay a substantial sum? Setting up an emergency plan could prove invaluable one day.

Need some help with business accounting and planning? Wootton & Co in the Lune Valley provide the full set of accountancy services including bookkeeping, corporate tax planning and VAT returns.

We support and advise our clients on many aspects of business finance and cashflow, so get in touch with us today.

New rules were introduced by the government last month which will impact contractors and self-employed people that do regular work for certain clients. Called IR35, this new legislation has been brought in to make sure that contractors pay the same amount of tax and National Insurance as they would if they were employed by their client.

It relates to an area called ‘off-payroll working,’ where contractors working through their own limited company – are acting as a permanent full-time or part-time employee of their client’s organisation.

What are the new rules?

As of 6th April 2021, the client who hires the contractor is responsible for determining whether their contractor is ‘inside IR35’ or operates ‘outside IR35’.

If a contractor provides services to a medium or large-sized private sector client, they will:

need employment status determination from the client, as well as the reasons why they made that determination

be able to dispute the determination given to them if they disagree

If you are ‘Inside IR35’

If the client feels you are operating ‘inside IR35’, you must pay the same tax as an employee. This could also mean that you are entitled to additional rights as an employee or worker (e.g. minimum wage, holiday pay, maternity pay, protection from discrimination). You may be offered an employment contract with your client.

If you’re found to be working inside IR35 but have not become an employee, you will usually have to pay at the end of the tax year any tax deductions or NIC that an employee would have paid.

Am I likely to be Inside or Outside IR35?

The Government has said this will not affect people who work as genuine freelancers. It is targeted largely at contractors who work for a single client for several months or years.

You’re more likely to be considered Outside IR35 if you:

• Work for multiple clients. • Are paid a variable amount month to month. • Are paid by the job rather than by the hour. • Can substitute your labour with another. • Market your services via a professional website. • Have your own business insurance and equipment.

You can check the specifics on the Government Website – there is also a Check Employment Status for Tax (CEST) tool to find out if you should be classed as employed or self-employed for tax purposes. Learning from the public sector

The same ruling was brought in purely for the public sector in 2017. Generally, it led to a reduction in the number of external consultants being taken on by public sector organisations.

I’m a contractor – how can I get around the IR35 legislation?

If you are concerned that IR35 will negatively affect your business, there are a couple of options:

1. Work with small businesses. There is no change to the rules for contractors providing services to small businesses in the private sector.

2. Work for an umbrella company If you are a self-employed contractor but operate under an umbrella company, you don’t need to worry about IR35. But being an employee of an umbrella company does not maximise your tax planning and there may be better alternatives.

3. Partner with other contractors One of the key checks is that you can substitute with other contractors and so an agreement with other contractors may eliminate this issue.

4. Negotiate new rates Some clients will be open to new ways of working to retain important contract resource. Note, however, that as an employee you may not be in a worse position. Contracts up to £10,000 can be more lucrative if performed as an employee. Not to mention the added protection and benefits employment brings.

Further help and support

For detailed tax advice and small business support, get in touch. David Wootton & Co are business tax accountants for small business owners like you – we can explore your specific situation and work out the most effective approach for your company.

David Wootton & Co – Lune Valley Accountants. Call us on 01524 236323 or email david@woottonandco.com

The 2021/22 tax year began on 6 April 2021, so we’ve pulled together a list of all the important tax information for businesses and individuals for the months ahead.

Personal Tax Allowance

Your Personal Allowance is the amount you can earn before you need to pay any Income Tax. The threshold has increased to £12,570 for this tax year, a small increase on last year’s allowance of £12,500. The rate of tax paid at this salary is 20%.

The threshold for Higher Rate income tax at 40% has increased by £270 to £50,270. These thresholds are now frozen until 2026.

What does this mean for Company Directors?

Based on these new thresholds, we recommend a salary of £8,840, with dividends of up to £41,430. This way, you will pay tax at 20% on take-home pay of £47,592.50 – your personal tax bill would be £2,677.50.

The Tax-Free Dividend Allowance for the tax year remains at £2,000. Dividend tax rates have not changed, but the thresholds increased as per the income tax thresholds above.

Basic-rate taxpayers pay 7.5% on dividends

Higher-rate taxpayers pay 32.5% on dividends

Additional-rate taxpayers pay 38.1% on dividends.

For tailored tax advice regarding your small business, just get in touch.

Personal tax relief and allowances

Personal Savings

The 0% starting tax rate remains at its current level of £5,000.

The adult ISA annual subscription limit remains the same at £20,000.

The annual subscription limit for Junior ISAs and Child Trust Funds is the same at £9,000.

Higher-income Child Benefit threshold

Since January 2013, people claiming Child Benefit must pay a charge if either member of a couple earns more than £50,000. This threshold is unchanged.

Personal pensions

The tax-free amount you can pay into a personal pension remains at £40,000. The lifetime allowance for pension savings remains at £1,073,100 and is frozen until 2026.

Capital Gains Tax

The Capital Gains Tax annual exempt amount remains at £12,300 and is frozen at this level until 2025/26.

Inheritance Tax

There is no change to the Inheritance Tax (IHT) nil rate band. The threshold remains at £325,000 and will stay the same until 2026.

Stamp Duty Land Tax

The stamp duty holiday for the first £500,000 Nil Rate Band of the purchase price will continue until the end of June 2021. From 1st July 2021, the Nil Rate Band will reduce to £250,000 until 30 September 2021 before returning to £125,000 on 1 October 2021.

Company Vehicles and Fuel Benefit

Company cars

Cars first registered after 5th April 2020 will see their Benefit in Kind charge increase by 1%. The percentage applied to the list price of the car will increase based on CO2 emissions published by the Vehicle Certification Agency. This HMRC has published a useful online company car tax calculator.

Fully electric cars have no tax charge this tax year, but next year will be charged at 1% of their list price, increasing to 2% in 2022/23.

Company vans

If you use company-bought fuel in a personal capacity, it is a Benefit in Kind. The tax on fuel benefit has increased as follows:

The BiK on company vans increases to £3,500 (from £3,490)

The BiK on fuel for a van for personal use increases to £669 (from £666).

This can be reduced under some circumstances – e.g. if the van isn’t driven for 30 days in a row or if you pay for private use of the van.

Fuel benefit for company cars

An employee who has a company car and free fuel from the employer is taxed on the cash equivalent value of the benefit each tax year. This has increased from £24,500 to £24,600.

Corporation Tax

Corporation tax remains at 19% of company profits but will rise to 25% from April 2023. At this point there will be a new ‘small profits rate’ of 19% for companies with profits of less than £50,000. The rate rises in line with profits above this level.

Businesses with profits over £250,000 will pay the full rate of 25% from April 2023.

Entrepreneurs’ Relief

Entrepreneurs’ Relief is now Business Asset Disposal Relief. It reduces Capital Gains Tax when you sell a business asset. The lifetime allowance limit remains capped at £1 million.

Information for Employers

National Minimum Wage and National Living Wage

The National Minimum Wage and National Living Wage amounts have increased to £8.91 per hour. It now applies to any adult aged 23 years and above.

Student Loans

The earnings thresholds above which you must start to repay a student loan have increased:

Plan 1 loans now £19,895 (was £19,390) Plan 2 loans now £27,295 (from £26,575)

A new Postgraduate Master’s Loan has been introduced by the government. It is repaid in the same way as any other Student Loan. Interest is charged from the day of the first payment. Repayment will be at 6% for students in England and Wales on income above £21,000.

Workplace pensions (auto-enrolment)

There are no changes to the minimum contribution for employees’ auto-enrolment workplace pension. The total of employer and employee contributions remains a minimum of 8% of the employee’s qualifying earnings.

Apprenticeships

The apprentice hiring incentive in England has been extended to September 2021. The payment has increased to £3,000. A new flexi-apprenticeship scheme will allow apprentices to work with multiple employers in a sector.

Eligible retail, hospitality and leisure properties in England will continue to receive 100% business rates relief from 1 April 2021 to 30 June 2021.

This will be followed by 66% business rates relief from 1 July 2021 to 31 March 2022, capped at £2 million per business for properties that were required to be closed on 5 January 2021, or £105,000 per business for other eligible properties.

Recovery Loan Scheme

The Recovery Loan Scheme will provide lenders with a guarantee of 80% on eligible loans between £25,000 and £10 million. The scheme will be open to all businesses, including those that have already received support under the existing COVID-19 guaranteed loan schemes.

The previous Coronavirus Business Interruption Loan Scheme (CBILS) and the Bounce Back Loan Scheme have now closed.

Restart Grants

New ‘Restart Grants’ to help businesses in England reopen from April 2021 include:

Up to £6,000 per premises for non-essential retail.

Up to £18,000 for hospitality and leisure venues that cannot open until later in the year.

Statutory Sick Pay

Small and medium-sized employers in the UK will continue to be able to reclaim up to two weeks of eligible Statutory Sick Pay (SSP) costs per employee.

Universal Credit and Working Tax Credit

The temporary additional £20 Universal Credit uplift will be extended by a further six months and also announced a £500 one-off payment for eligible Working Tax Credit claimants.

Need some support?

For a discussion about what these rules mean for your business, get in touch. Here at Wootton & Co we take time to explore all the options for our clients. Our accountancy services include personal tax planning, business accounting and payroll. Contact the team to find out why we’re a trusted Lune Valley Accountant for companies large and small.

I will be updating with news that will affect small to medium size businesses

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.